PaymentIntelligence – When payments intersect with artificial intelligence, blockchain, and data science, we step into a new era—Payment Intelligence. This fusion brings forth a revolution in the payments ecosystem, combining cutting-edge technologies to create efficient, secure, and scalable solutions.

In today’s world, both developing and developed economies require payment methods tailored to their specific needs and environments. Whether it’s through mobile wallets, contactless payments, or cross-border solutions, there’s no one-size-fits-all approach. This diversity in payment channels highlights the importance of flexibility and adaptability, especially in a fintech-driven landscape.

At the core of Payment Intelligence is a shared goal: eliminating corruption and inefficiencies, which often stem from cash-based systems. Cash remains a vulnerability for businesses and governments, creating opportunities for fraud, tax evasion, and money laundering. The answer lies in intelligent payment systems that leverage advanced technologies to offer transparency, traceability, and accountability.

This post is an extract from my presentation done at the GECommunity 2017 Summit in Kuala Lumpur, Malaysia. The GE Community Summit is an annual event that attracts the best and brightest talents from academia as well as industry.

The Payment Intelligence (PI) System is the cornerstone of this Financial Services Internet i.e. Finternet, transformation, integrating real-time data analytics, AI-driven decision-making, and blockchain’s immutable ledger to streamline payments while enhancing security. As a hands-on technology leader, I’ve seen firsthand how this shift from cash to digital can transform industries—helping businesses scale, governments regulate, and customers experience seamless, secure transactions. In short payments that can think before they move — each transaction is a micro-decision engine, guided by data, intent, and context.

Payments: From Barter to Payment Intelligence

If you’ve been in financial technology long enough, you know that payments aren’t just about moving money — they’re about moving trust. I have seen payments evolve from the simplicity of barter and paper to the speed of electronic rails, and now into something almost self-aware — intelligent, adaptive, and autonomous.

In the early days, payments were dumb pipes — push and pull mechanisms where the human did all the thinking. Then came automation, digitization, and real-time rails that made money move faster than thought. But speed without understanding was never enough. What we needed — and what we’re finally building today — is Payments with Intelligence.

Introducing AI in Payments

Artificial Intelligence entered the payments ecosystem quietly, almost humbly — first as a fraud detector, then as a risk assessor, and now as a decision-maker. It watches, learns, predicts, and optimises. Every transaction becomes a data point, every pattern a signal, and every anomaly an opportunity to protect or personalise.

| Era | Nature | Human Role | System Role |

|---|---|---|---|

| Barter & Paper | Manual & Trust-based | 100% Human | None |

| Electronic | Digital & Rule-based | Operator | Processor |

| Autonomous | Automated & Event-driven | Supervisor | Executor |

| Intelligent | Contextual & Predictive | Partner | Thinker |

| Agentic | Self-learning & Self-deciding | Collaborator | Co-creator |

AI didn’t just improve payments; it gave them eyes and ears. It’s no longer about “processing” — it’s about interpreting and adapting in real time.

The Birth of Payments Intelligence

Payments Intelligence is where data, AI, and finance finally speak the same language. It’s the fusion of transaction analytics, behavioural modelling, and contextual awareness — the moment when money starts thinking for itself.

Two Things That Define the Future

- Human-AI Collaboration: Payments will not replace humans — they will represent them, carrying our intent, context, and trust across networks.

- Intelligent Payments: The next decade belongs to payments that act — not on instruction, but on understanding, i.e., can think before they move. Each transaction will be a micro-decision engine, guided by data, intent, and context.

The journey from barter to bytes to brains has not just been technological — it’s been philosophical. Payments have grown from being a means of exchange to being a medium of intelligence. The systems we build today are not just rails or APIs; they’re reflections of how we, as humans, define value, trust, and fairness in a connected world.

In PI world, payments don’t just happen, they negotiate, decide, and learn. They understand when to pay, how to pay, and even why to pay. They evolve from being transactional to being intentional.

Artificial Intelligence in the Payments Industry

Having more data from digital payment transactions not only helps prevent fraud but also contributes to human health by reducing exposure to bacteria and viruses found on physical currency. Yet, the growing volume poses a challenge for fraud-detection systems. To address this, integrating machine learning into the digital money system boosts its abilities. Trained algorithms and data models excel at spotting anomalies and unusual fraud patterns that might escape human detection.

The current payment system or typical traditional digital payment system has too many limitations and static or rigid variables like merchant type, currency code, country code, location, product type, usual spending range, etc. tied to users. These attributes are almost impossible to change or adjust in an automatic manner, as there is no learning curve. So as the user or customer behaviour changes, the system has no velocity to adjust but just raises or blocks it as potential fraud.

Payments wrapped in AI (machine learning), so-called payment intelligence, improve threat hunting and fraud detection significantly. score-based risk assessment and then adjusting the scores and learning from user behaviour, i.e., spending amounts over a period of time, changes in spending locations, etc. Online transactions with different source IPs and physical distances between transaction originating IPs are a few examples that machine learning can pick and analyse much better and faster. Machines can decide to send OTP in case second-level authentication is needed, and mobile phone cell ID would be an awesome combination there.

PaymentIntelligence a New Dimension

PI at the national level can bring the whole nation together. It can secure the economies and flush out the underground economies. In a scenario where you are in a shopping mall and get an SMS, That reads “Walk on to the 3rd floor to buy your favourite brand of clothes to get a 20% discount”.

Because it’s the 25th of the month and you got paid, meaning you have money. So here, merchants, banks, employers, telephony service providers, credit service providers, and many others are all connected to the PI system, so this kind of system can generate business. In the US alone, real-time payment eventually became the first new core payment infrastructure, the most advanced in more than 40 years.

Now a second scenario on top of the first one: “you fall short in your balance system to make payment”. In this system case, the payment intelligence system can offer microcredit of $10 to $500, depending on your credit rating. Even if the system charges you a 10–20% rate of interest for a 3-month period (80% over 12 months), you won’t even mind or make the note.

PaymentIntelligence (PI) System: Can open a lot of opportunities to young entrepreneurs and boost the economy of the nation. Data alone is lifeless and inherently dumb. It doesn’t do anything alone without support, knowledge, and tools on how to use it and how to act on it. Algorithms are where the real value lies. Algorithms define and drive actions. The whole point of the PI algorithms involved in high-frequency business is to detect, analyse, and make decisions faster than a human heartbeat.

Unlocking Payment Data Intelligence – Intelligence Hub

Working with payment data today is more complex than ever before. One of the challenges I’ve faced firsthand is the need for data fabrication to bridge the gap in data intelligence and efficiency. Converting raw, siloed data into a trustworthy flow that anyone can use is a monumental task. But once it’s done, the value it unlocks is huge.

AI is the key to enabling organizations to access trusted data faster and make decisions with greater confidence. In my experience, AI-driven payment systems offer tremendous benefits for both customers and businesses, and it’s impossible to overstate how transformative these systems can be. Payment data intelligence, in particular, brings several key advantages:

- Ensure Trusted Data from the Start: With a strong Data Inventory, we can ensure that the data we rely on is trustworthy, from the very first interaction.

- Boost Efficiency and Productivity: With tools like Pipeline Designer, we can dramatically increase our ability to process and manage data, making workflows smoother and faster.

- Automate Integration Tasks: AI and APIs come together to automate tasks that once required manual effort, freeing up resources for more strategic work.

Payment intelligence is transforming financial services in ways we’ve never seen before. From payment systems to clearing and financial settlements, this shift is paving the way for new, powerful products. Data inventory creators, alongside machine learning algorithms, are modernizing data engineering, accelerating the adoption of smarter, more efficient systems. When we adopt Payment Intelligence (PI), we’re not just modernizing how payments work—we’re building the foundation for a more transparent, fair, and efficient global economy. The future is already here, and with the right tools, we can be at the forefront of this change. Together, we can unlock a world of possibilities for businesses, consumers, and markets around the world.

Cognitive Payments: The Future of Payments Intelligence

Cognitive Payments represent the next evolution in the payments industry, leveraging advanced technologies like artificial intelligence, machine learning, and cognitive computing to create smarter, more intuitive, and secure payment ecosystems. At the heart of this transformation lies Payments Intelligence, a framework that uses data-driven insights to enhance decision-making, optimize processes, and deliver personalized experiences.

| Feature | Description | Example |

|---|---|---|

| Data-Driven Insights | Relies on vast amounts of transactional data, user behavior, and contextual information. Payments Intelligence systems analyze this data in real-time to identify patterns, trends, and anomalies. | Detecting fraudulent transactions by recognizing unusual spending patterns or geographic inconsistencies. |

| AI and Machine Learning | AI algorithms power predictive analytics, enabling systems to anticipate user needs and preferences. ML models continuously learn from new data, improving accuracy in fraud detection, risk assessment, and customer segmentation. | Suggesting payment methods based on past behavior or optimizing cash flow for businesses. |

| Natural Language Processing (NLP) | NLP enables conversational interfaces, such as chatbots or voice assistants, to facilitate seamless payment interactions. | “Pay $50 to John for dinner using my credit card.” |

| Real-Time Decision-Making | Cognitive Payments systems process transactions in real-time, making instant decisions on authorization, fraud prevention, and routing. | Approving a high-value transaction while flagging it for additional verification if it deviates from the user’s typical behavior. |

| Personalization and Context Awareness | Payments Intelligence systems use contextual data (e.g., location, time, device) to tailor payment experiences. | Offering discounts or loyalty rewards at the point of sale based on the user’s preferences and purchase history. |

| Blockchain and Smart Contracts | Cognitive Payments can integrate blockchain technology for enhanced security, transparency, and automation. Smart contracts enable self-executing payment agreements, reducing the need for intermediaries. | Automating subscription payments or supply chain settlements based on predefined conditions. |

The Future of Cognitive Payments

As Payments Intelligence continues to evolve, Cognitive Payments will become more pervasive, integrating with emerging technologies like the Internet of Things (IoT) and 5G networks. Imagine smart devices autonomously making payments (e.g., a refrigerator ordering groceries) or seamless cross-border transactions powered by AI-driven currency conversion and compliance checks.

In essence, Cognitive Payments, powered by Payments Intelligence, are transforming the payments landscape into a smarter, more connected, and user-centric ecosystem. By combining data, AI, and real-time decision-making, they are redefining how we pay, interact, and transact in the digital age.

Desired Outcomes for PI Systems

One of the most exciting aspects of PI systems is the opportunity to bring together technical and business minds who understand the potential of AI. By aligning these two perspectives, we can create innovative products and solutions in the financial technology and banking sectors. Payment intelligence offers fresh opportunities to build strong, secure, and thriving national payment systems. It holds the potential to revolutionize the convenience and security of digital currency on a global scale.

- Reducing Cyber Fraud Risk: PI systems play a critical role in minimizing the risk of cyber fraud by identifying and preventing fraudulent activities early.

- Importance of Robust Security: Security is vital for merchants, financial institutions, and consumers, and PI systems provide the tools to ensure a secure transaction environment.

- Early Detection and Prevention: The fraud management module in PI systems empowers stakeholders to address payment issues before they escalate, mitigating compromised payments.

The FinTech space has grown exponentially, and last year alone, it received $19 billion in venture capital investment. This growth is driven by best practices—rapid response, triage, and preventive analysis from technical forensic investigations. With a PI system, we gain the ability to conduct cyber analysis and build out infrastructure for digital money platforms, fortifying the system against potential threats.

Smart Tech is here to Empower Everyone. Smart technology in finance, like Payments Intelligence, is no longer a luxury reserved for the tech elite. It’s the foundation of modern FinTech’s promise to deliver hyper-personal, simple, and secure experiences. By harnessing the power of Smart Tech i.e. Intelligent Tech (AI, ML etc) and Trust Tech (Blockchain & HLT) , the industry is rewriting the rules, putting you at the heart of innovation and business growth.

FinTech & AI – Payments with Artificial Intelligence.

FinTech intelligence can help in one way or another how to make money. The application of any computer-enabled algorithm that can be applied against a data set to find a pattern in the data Because of this, new wild and flashy AI systems are making FinTech’s smart systems smarter and can help them to fly. Not surprisingly, these companies each have a clear market application and reduce friction in the business problems they address.

Fintech’s Artificial Intelligence Revolution is a perfect example and era of pervasive AI financial technology services. The aim of payment intelligence is to explore AI potential in the financial sector and to become a major business disruptor. The AILabPage team did a small research project with its freelance members on a global practice that designs and implements digital transformations.

AI Boosting Info-security with Behavioural Biometric

In my hands-on work with the FinTech industry, I’ve seen firsthand the tremendous opportunities AI brings in enhancing decision-making. Whether it’s improving lending decisions, optimizing financial advising, or executing more informed trading strategies, AI can revolutionize these processes.

By improving the algorithms, we can create more accurate, efficient, and personalized financial advice for users, elevating their experience while mitigating risk.

- The Growing Need for Better Security – The rise of account takeovers and mobile fraud has brought a growing urgency to move beyond traditional password protection and two-factor authentication. In this age of relentless cyber threats, hackers continuously find ways to steal personally identifiable information (PII), leaving systems vulnerable. This is where Behavioral Biometrics (BBI) can truly make a difference.

- Simplifying Transactions with BBI – With BBI, consumers will soon be able to complete complex transactions—like making purchases, transferring funds, or processing payments—without ever needing to type a single character. It’s like a seamless, invisible layer of security, quietly working behind the scenes.

- Innovative Approach to Security – Behavioral biometrics presents a fresh approach to monitoring and scoring customer interactions with devices during transactions. Unlike the rigid, password-based security we’ve relied on, BBI leverages real-time user behavior patterns to authenticate actions and detect anomalies, offering a dynamic way to protect sensitive data.

- Voice Biometrics and Emotional Understanding – Then there’s voice biometrics, an exciting area where AI and voice technology converge. Imagine a future where AI can understand not just the words you speak but the emotions behind them. By combining this with voice-enabled chatbots, we could reduce reliance on human operators in call centers and simultaneously protect sensitive data from internal leaks. It’s a powerful move toward a more efficient and secure customer service experience.

- Adapting to a Dynamic Digital Landscape – As the digital landscape continues to evolve, businesses must adapt to this growing complexity. The integration of AI, BBI, and voice biometrics will require a dynamic blend of technologies, disciplines, and practices. And as technology advances, it’s crucial for organizations to not only adopt the right tools but also invest in developing their teams’ skills to fully harness these innovations.

I’m excited to be part of this journey as we reshape the future of secure, seamless, and intelligent financial services.

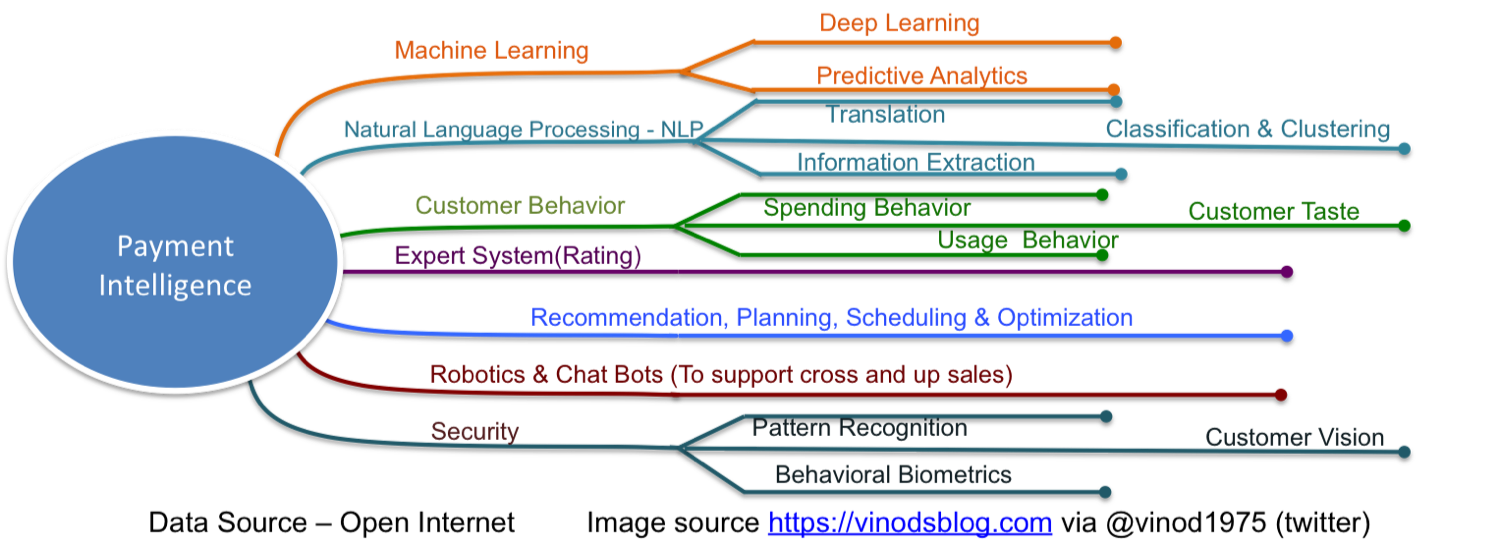

PaymentIntelligence is a new dimension of payment science that combines artificial intelligence, blockchain, data science, and machine learning as its foundation.

Banking Applications with Artificial Intelligence

Application Artificial intelligence has several applications in the banking industry. Top-5 applications of artificial intelligence in the banking industry that will revolutionise the industry in the next 5 years are listed below.

| Technology | Applications | Security Threats & Challenges |

|---|---|---|

| Algorithmic Trading | Automated, data-driven trading strategies to optimize stock market outcomes. | Potential security risks from algorithm manipulation and market abuse. |

| Chatbots | AI-driven virtual assistants for improving customer service and engagement. | Vulnerability to malicious scripts or exploitation through chatbot interfaces. |

| Customer Recommendations | Personalized product suggestions based on customer data and behavior analysis. | Risk of data breaches exposing personal customer preferences. |

| Fraud Detection | AI and machine learning techniques to identify unusual patterns indicating fraudulent activities. | False positives, incomplete data, or evolving fraud tactics may compromise accuracy. |

| AML Pattern Detection | Monitoring and identifying patterns linked to money laundering activities. | Sophisticated methods might bypass detection algorithms or cause delayed alerts. |

| Blockchain | Decentralized digital ledger offering transparency and security for transactions. | Threats such as application tampering, rogue apps, malware, and overlay attacks. |

| Business Strategies Impact | Strategic decisions may be jeopardized by weak security and compromised tech infrastructure. | Application tampering, rogue apps, malware, overlay attacks, and other threats. |

Artificial intelligence is ready for business but the business may not be ready for AI, this where the major issue is. AI hype putting almost every business in peril and many businesses are now forced to make claims then real work.

Intelligent tools for Threat Intelligence / Threat Hunting.

What is needed in today’s payment market is an intelligent system to do automatic threat intelligence. The system can perform threat hunting without rest in a 24/7 manner. Blockchain will also push PI (payment intelligence) system demand towards the north at rapid speed.

Why blockchain when we have AI as a supportive partner in the payment system? The response is actually out of scope for this post, but for now, we can learn it has an important role for payment security reasons. As of date, 40% of the banks find themselves still in the exploration phase of blockchain technologies. While around 30% are pursuing proof of concepts, These are not at all good signs.

Evolution: Barter → Paper → Electronic → Autonomous → Intelligent → SelfControl(Think & Talk)

intra-bank cross-border transactions are regarded as the most likely payment system to see blockchain implementation, followed by cross-border remittance and corporate payments. PaymentIntelligence brought real-time payment which eventually brought real-time threats as well. P2P and m-commerce payments are fuelling growth in real-time payment systems.

PaymentIntelligence as a Service

One of the technologies which have received considerable hype in recent years is blockchain. A distributed ledger technology (DLT) that serves as the backbone of cryptocurrencies. Application development technologies and disciplines continue to evolve as the need to deliver business outcomes and accelerate application delivery with high quality intensifies. Blockchain’s financial part underpayment intelligence encompasses all types of data science algorithms, supervised, unsupervised, segmentation, classification, and regression including deep learning.

That’s simplistic for a reader to appreciate the importance of Regression. Historical notes on Knowledge discovery and data, CRISP-DM, BIG DATA, and Data Science and their relationship to data mining and Machine Learning are available all over the internet for free. How to put them in real business and discover the hidden potential of such powerful tools to bring values are still not much talked or explored.

Please note I am not advocating AI on blockchain here as the basic architecture for both as per my understanding is a lot different as on date. Also, Deep Learning is different from traditional predictive analytics in my opinion hence my picture above shows the same.

Smart machines producing smart payments with inbuilt payment intelligence. What fascinated me most in PI subject book (Currently being written) the explanation of such complex subject, regression and use of AI and its components. They are described as ‘ a tutor teaching students in an institute – if the outcome is continuous use linear and if it is binary, (Regression) use logistics.

New Job role Payment Intelligence and SECaaS Analysts

Soon in the market or it must have started already in the market in payments and info-security industry to fight cyber-crimes. These professionals will be a great value add to

- Serve as a Global Risk Subject Matter expert on various payment frauds via new brand new platform i.e payment intelligence.

- The new system or PI says will be able to analyse data and respond to alerts relative to SECaaS as the built-in metric.

- Statistics & machine learning techniques surrounding cybercrime case will report and investigated in an automatic manner.

These professionals will lead the design and production deployment of new and advanced techniques to recognise and prevent payment methods and cybercrime.

About the Summit

The summit took place on 12th and 13th December 2017. This was the biggest summit in Malaysia and the opening speech was done by “Sri Haji Mohammad Najib bin Tun Haji Abdul Razak”. Sri Haji is the current Prime Minister of Malaysia since 2009. The event was attended by almost 15,000 participants with speakers from 27 countries around the globe.

If anyone is looking for a complete and detailed presentation free copy, please leave your email address in below comment box. I will talk about different elements of PaymentIntelligence (PI) in this post on a very high level only. The idea is to show what is PI, what it can do and what all elements are in the ecosystem of PaymentIntelligence.

Conclusion – Artificial Intelligence isn’t just transforming global finance — it’s rewriting the FinTech story altogether. In Africa, the shift is even more dramatic. Over the past five years, we’ve seen AI converge with mobile money ecosystems like M-Pesa, Airtel Money, and others to power smarter merchant payments, bill payments, and prepaid services. This continent already runs on one of the world’s most advanced mobile payment infrastructures — ultra-modern, scalable, and deeply embedded in daily life.

Now imagine layering AI on top of that — from predictive credit and fraud analytics to conversational banking and real-time compliance. In short, Payments that can think before they move — each transaction is a micro-decision engine, guided by data, intent, and context. That’s where the next FinTech leap is happening — right here in Africa.

—

Disclaimer

All credit and credits of contributions remain with original authors and I sincerely thank for their contribution here. Welcome to the future of Payments. In this post, we have discussed the potential merger of AI and its bundle pack i.e. Machine Learning, data science and analytics. In the next post, we will pick up a specific use case to deliberate on.

#PaymentIntelligence #MachineLearning #DataIntelligence #DeepLearning #ArtificialIntelligence

Points to Note:

it’s time to figure out when to use which tech—a tricky decision that can really only be tackled with a combination of experience and the type of problem in hand. So if you think you’ve got the right answer, take a bow and collect your credits! And don’t worry if you don’t get it right.

Feedback & Further Questions

Do you have any burning questions about Big Data, AI & ML, Blockchain, FinTech, Theoretical Physics, Photography or Fujifilm(SLRs or Lenses)? Please feel free to ask your question either by leaving a comment or by sending me an email. I will do my best to quench your curiosity.

Books & Other Material referred

- AILabPage (group of self-taught engineers/learners) members’ hands-on field work is being written here.

- Referred online materiel, live conferences and books (if available)

============================ About the Author =======================

Read about Author at : About Me

Thank you all, for spending your time reading this post. Please share your opinion / comments / critics / agreements or disagreement. Remark for more details about posts, subjects and relevance please read the disclaimer.

FacebookPage ContactMe Twitter ========================================================================

Very insightful and I like the academic approach.

Excellence and exception is clearly seen here pls let me know how much the paid and full version of this ppt is … Send me the email for cost…. I know no free lunch in this world…..

very nice and excellent, this is going to be the future technology.. pls share me your presentation..

very insightful……

Please share the presentation

Very nice and insightful.please share the ppt

email address ??

nice article, could you please share full ppt to me ?thanks

Thanks for kind words, unable to locate your email address

Very insightful, can you share me the ppt to himawanisme@gmail.com? Thanks

Hi Vinod, I would like a copy of the presentation.

email address pls

Thank you for this post.

Please, share the presentation. anamakharadze94@gmail.com

Sent

Very good post regarding AI in business. Please share the ppt.

Thanks for kind words, unable to locate your email address

[…] Blockchain and Digital Payments – PaymentIntelligence […]

[…] All credits if any remains on the original contributor only. You can find our other post on payment intelligence “The new Intelligence in the market – PaymentIntelligence“ […]

Excellent approach Vinod, you have done a great research to achieve this information. Can you share me the presentation to my email? It’s sidney.28.03@gmail.com. Thanks.

sent

Very insightful. Kindly share the presentation on enrohit@gmail.com

Many thanks.

Very useful information. Could you please share your updated powert point?

My email address is: ldejoie@gmail.com

Thanks and regards.

[…] Original post: https://vinodsblog.com/2017/12/13/the-new-intelligence-in-market-paymentintelligence/ […]

[…] This is part 2 of the previous post from 2017 “PaymentIntelligence – Artificial Intelligence in the Payments Industry” […]

[…] Payments-driven models: It revolve around the facilitation of secure and user-friendly payment solutions catering to both individuals and businesses. These models are designed to provide convenient and reliable options for digital payments, mobile wallets, and other electronic transaction systems. […]

[…] in 2017, I introduced PaymentIntelligence and Cognitive Intelligence in payments, envisioning a world where AI could think, decide, and execute transactions […]

[…] Tech is here to Empower Everyone. Smart technology in finance, like Payments Intelligence, is no longer a luxury reserved for the tech elite. It’s the foundation of modern FinTech’s […]