Digital Payments Signature: Powerful Payments tool

This technology is crucial in combating fraud and building trust in digital transactions, as it enhances security and facilitates seamless financial interactions. As the digital payment landscape continues to evolve,…

Future of PaymentIntelligence with Embedded Lending, Investment and Insurance

The future of payment intelligence holds great potential with the integration of embedded lending, investment, and insurance. As technology advances and reshapes the financial landscape, the convergence of these services…

Payment Intelligence: Efficiency and Security in Cross-Border Payments

Payment Intelligence represents a watershed moment in the world of cross-border payments. It marries efficiency and security, unlocking new possibilities for businesses, individuals, and economies worldwide. As this transformative force…

The Hidden Forces: Exploring Physics and Blockchain in PaymentIntelligence

Payment intelligence, physics, and blockchain are combining to improve financial systems by using their unique capabilities. These technologies work together to provide a powerful synergy in which payment intelligence uses…

Payment Intelligence | Powerful And Strong Combo With AI

The fusion of Artificial Intelligence technology with payment processes has led to a remarkable enhancement in efficiency, creating a mutually beneficial partnership between the two domains. Artificial intelligence was acknowledged…

Digital Wallets and Security – Payments Landscape

If sensitive data is left unprotected, it can result in severe consequences for the service provider's business, including financial fraud, violations of legal regulations, penalties from the regulators, loss of…

AI Changing FinTech Modus Operandi

AI in Fintech is a great help & ease for understanding on how the automation can be achieved for automated tasks (yes its true). Machine Learning focuses on predictions, based…

AI: Transforming eCommerce into a Smarter and Powerful Shopping House.

In our todays online shopping how much is artificial intelligence. How artificial intelligence can help retailers to deliver the highly personalized experiences shoppers desire. Ant colony optimization algorithm (To formulate…

Artificial Intelligence Innovation in FinTech

With advancement in technology, artificial intelligence, organisations outside the banking industry diversified and demystified financial services by targeting small & succinct margins in the space. These were organisations servicing millions…

Artificial Intelligence for Digital Payments Security

The best to protect data from stealing by hackers; may be by not converting and putting the data in system, In the old days people says keep smiling it does…

Privacy, Innovations and Security in Digital Payments

Against escalating security threats on mobile payments, empowerment of merchants, acquirers, and service providers with new commerce opportunities and experiences in store and protection should

Digital Payments – Security vs Speed

Abstract – In Digital payments world million dollar question comes in at every stage what is more important security or speed (Performance & Ease). Financial system security design principles can…

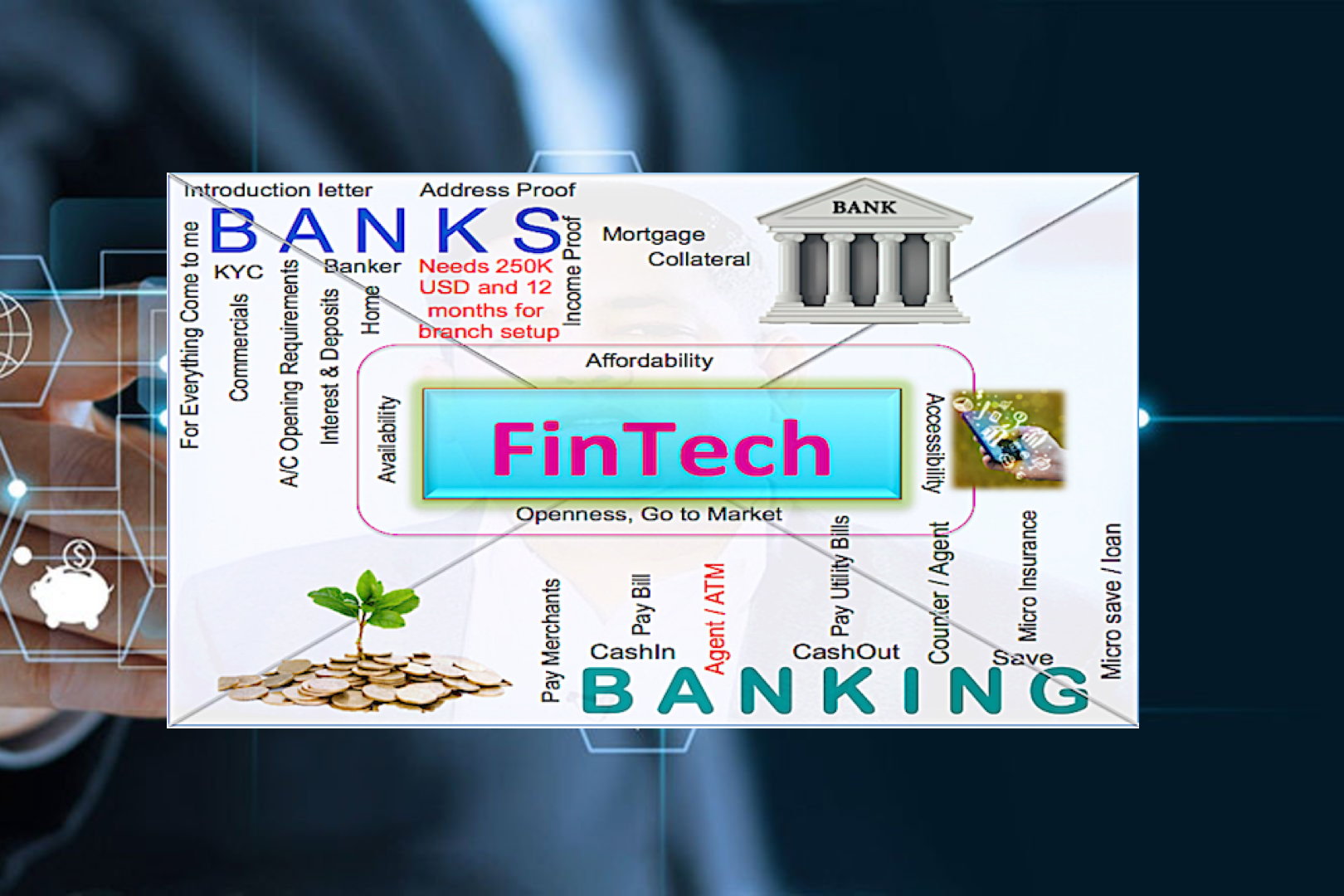

Digitised Bank Payments – Their Struggle Saga with Friend FinTech

MNO’s speed to achieve their goal to standardise, automate, digitise, remove boundaries by brining cross order financial/remittances service in form of payments, cash, airtime, paperless and online. At the same…

FinTech – A True Fairytale

Almost all players who entered into payments in arena of FinTech domain are actually coming out of this game park with zero or no knowledge. This is giving too much…

Year 2016 : What is needed, Banking or Banks?

"Banking is needed not the banks, Fintech is killing banks, not the banking". Banks need to accept change, become Fintech partners and it's time to come out of their 100-year…